Most coworking and flex space operators do not have a software problem. They have a workflow problem.

The tools are there. But too many everyday jobs still need manual help: fixing invoices, stepping into bookings, pulling reports, and switching between systems to finish one task.

That is the clearest takeaway from our latest UK coworking and flex space industry research.

According to CoworkingCafe’s Q1 2026 market report, the UK now has 4,270 flexible spaces. This is already a large, competitive market. In a market like that, operational drag matters. The teams that spend less time on admin have more time for sales, community, occupancy, and better decisions.

This piece combines a focused survey of UK coworking and flex space operators with broader insights from around 200 operator conversations through FlexSA and London Coworking Assembly events, direct calls, and in-person visits to coworking spaces across the UK. It also adds market context from the Instant Group’s UK flex market overview.

Prefer a shareable version? Download the full PDF version of this UK coworking operator research.

Quick answer: what is still slowing coworking operators down?

Not a lack of software.

The bigger problem is that many operators still need to do manual work around:

- billing

- bookings

- reporting

- cross-system workflows

In this research, that showed up in five clear findings:

- 63% use 2–3 apps to run their space

- 75% still manually fix billing or invoices at least sometimes

- 50% still cannot fully self-serve bookings, catering, and guests

- 71% cannot instantly see their most profitable room or resource

- if teams got 10 hours back per week, they would spend it on sales and marketing or events and networking

That is the story in one line: operators do not want more features. They want less friction.

What operational friction means in coworking

In this context, operational friction means the extra admin that shows up when software and processes still need human intervention.

It usually looks like this:

- staff stepping in to fix invoices

- bookings that still need front-desk help

- reporting that requires CSV exports and spreadsheet cleanup

- teams switching between multiple apps to complete one workflow

None of that sounds dramatic on its own. Together, it adds up fast. It slows teams down, makes systems feel less trustworthy, and pulls time away from the work that actually grows the business.

Why this matters more in 2026

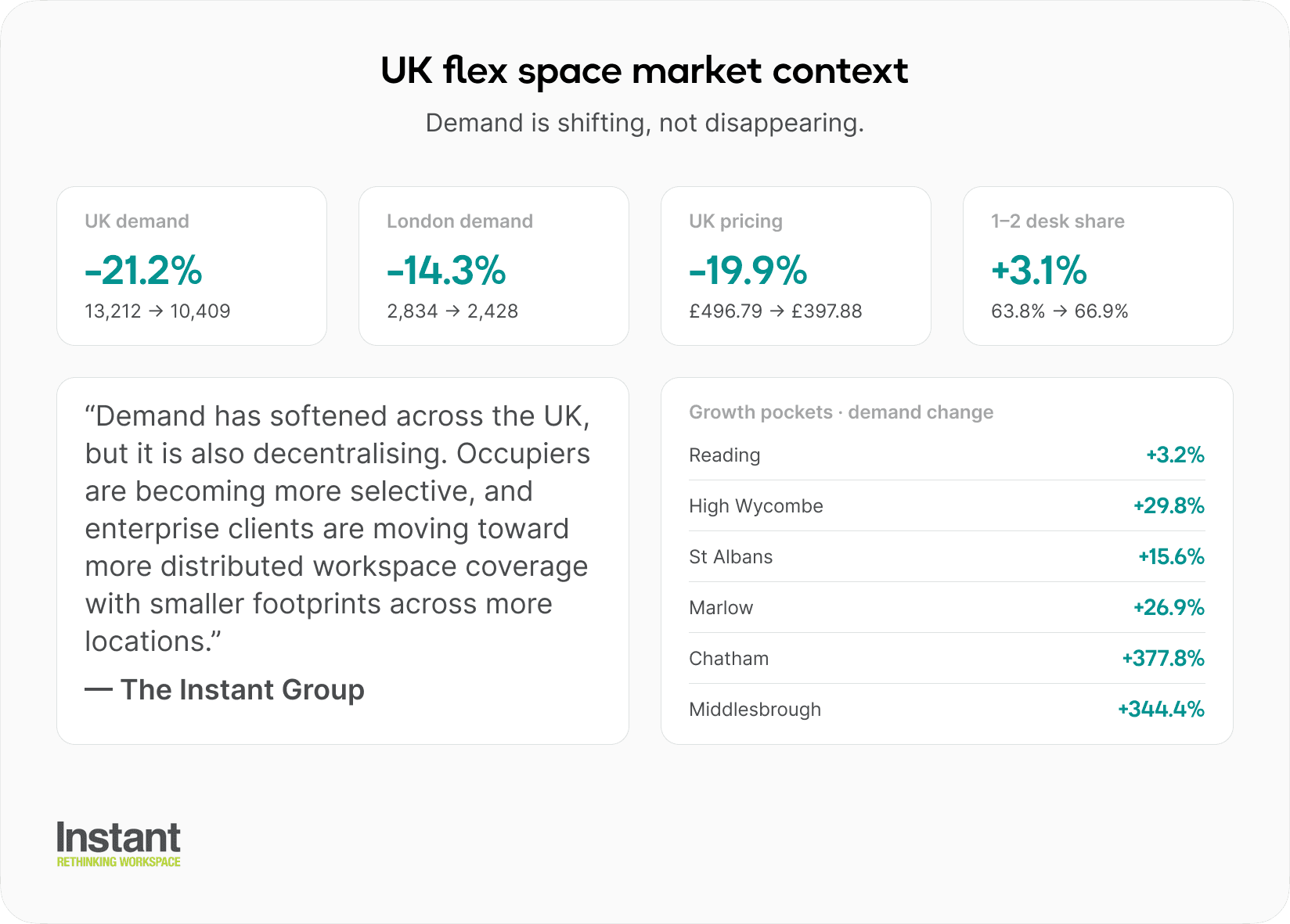

The survey findings matter on their own. But they matter more when you place them next to what is happening in the wider UK flex space market.

Based on the Instant Group’s market overview:

- London demand in the dataset fell from 2,834 to 2,428 (-14.3%)

- some commuter and regional markets grew sharply, including Reading (+3.2%), High Wycombe (+29.8%), St Albans (+15.6%), Marlow (+26.9%), Chatham (+377.8%), and Middlesbrough (+344.4%)

- average UK pricing in the dataset fell from £496.79 to £397.88 (-19.9%), while some regional cities still saw growth, including Glasgow (+21.6%), Liverpool (+11.2%), Leeds (+8.5%), and Reading (+5.9%)

- smaller requirements are becoming even more dominant: 1–2 desk demand increased from 63.8% to 66.9% of requirements in the dataset

Data and insights provided by The Instant Group are compiled from their proprietary flexible industry database, providing a comprehensive, aggregated market view of flex market demand.

This is not just a decline story. It is a redistribution story. Demand is moving across locations, buyers are becoming more selective, and smaller requirements are becoming a bigger part of the market.

That makes everyday operational clarity more important, not less. If demand is shifting, operators need to know where they are making money, where they are losing time, and which workflows still depend on staff stepping in.

The Instant Group put it like this:

“Flexible workspace demand has softened across the UK, with a 21% dip in Q1 2026 compared to the same period last year.

However, this is not a broad trend as demand is instead decentralising and occupiers are becoming more selective in their office usage.

While many large cities have seen a drop in demand, pockets of growth are evident, in particular in towns with strong rail links to London which offer a more cost effective London spillover solution, for example Reading, High Wycombe, St Albans and Marlow.

Growth is also evident in regional growth hubs and regeneration hubs such as Chatham and Middlesbrough.

Enterprise clients are now changing how they use office space and are moving towards more distributed workspace coverage, adopting smaller footprints across distributed locations. As a result, demand is shifting towards a larger proportion of smaller requirements and a smaller proportion of larger requirements.”

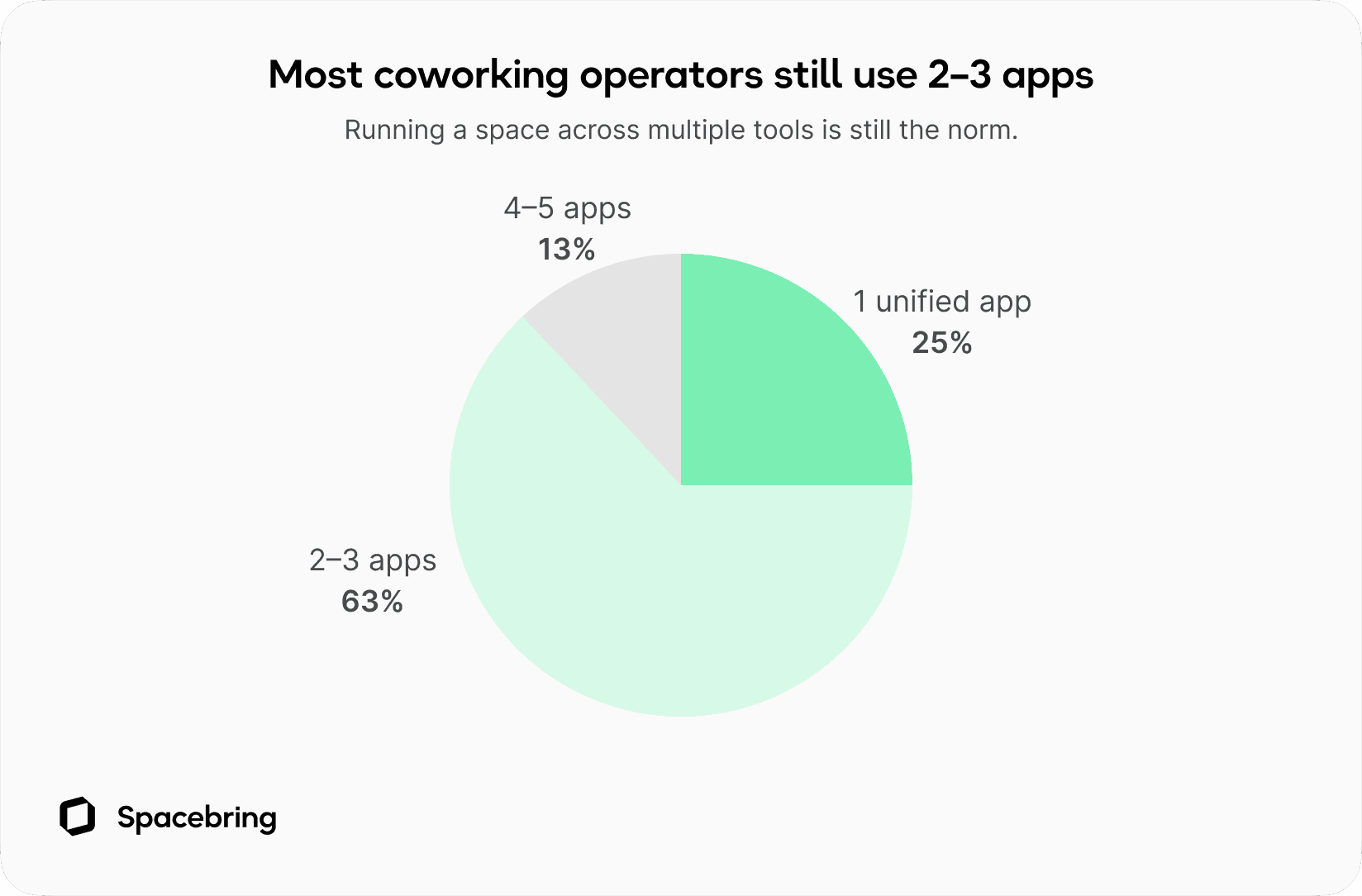

1. Most coworking operators still use multiple apps

Percentages may not total 100% due to rounding.

We asked:

How many apps does it take to run your space?

Here is what operators told us:

- 25% use 1 unified app

- 63% use 2–3 apps

- 13% use 4–5 apps

The most common answer was 2–3 apps.

That may not sound surprising. Plenty of operators accept multi-tool setups as normal. But every extra tool adds another login, another handoff, another place where data can drift out of sync, and another point where routine work gets slower.

Using multiple apps is not automatically bad. The problem starts when people have to stitch them together manually.

What this finding means

App sprawl is easy to shrug off because it rarely breaks everything at once. It just makes the whole business heavier over time.

That shows up in billing, reporting, staff training, support, and everyday decision-making.

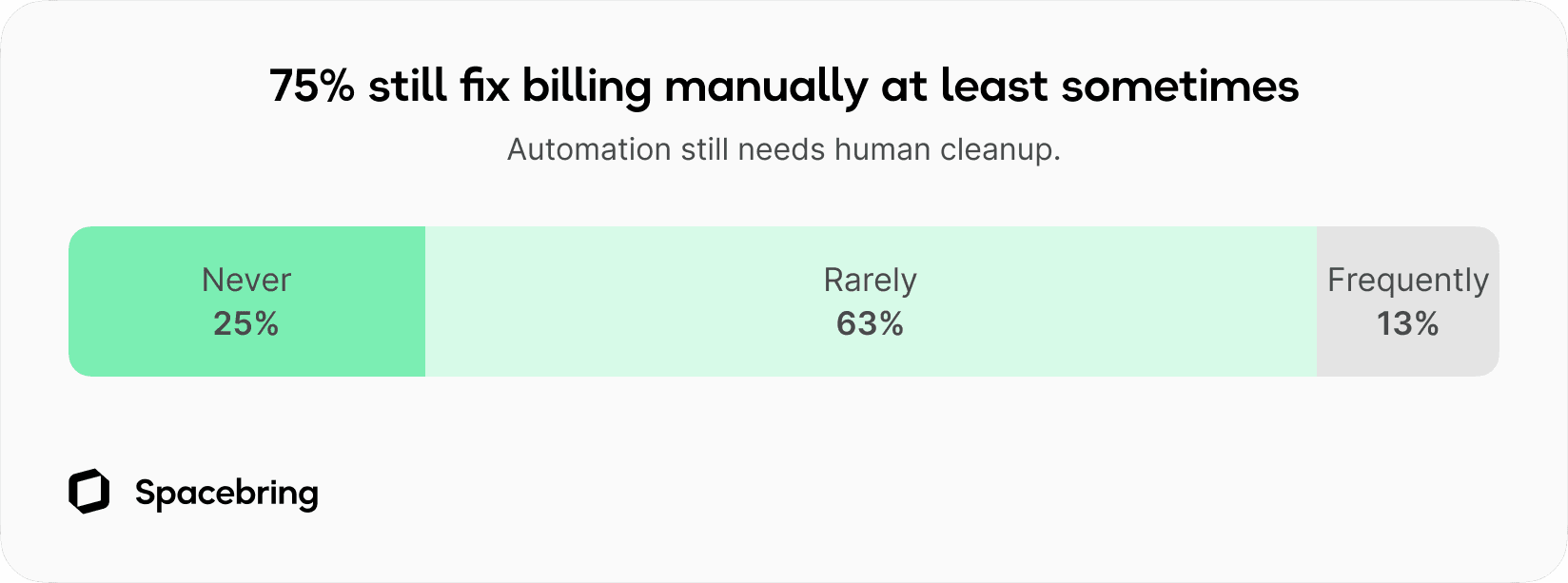

2. Billing still is not truly hands-off

Percentages may not total 100% due to rounding.

Next, we asked:

How often do you manually fix your automated billing or invoices?

The responses:

- 25% said never

- 63% said rarely

- 13% said frequently

So 75% still step in manually at least sometimes.

That is one of the clearest signals in the research.

If automated billing still needs checking, correcting, or cleanup, it is not really hands-off. It is partly automated and partly supervised.

What this finding means

The cost is not just the minutes spent fixing invoices. It is also the background mental load.

If operators still have to wonder whether billing ran properly, that system is still asking for attention. Once a system keeps asking for attention, people stop fully trusting it.

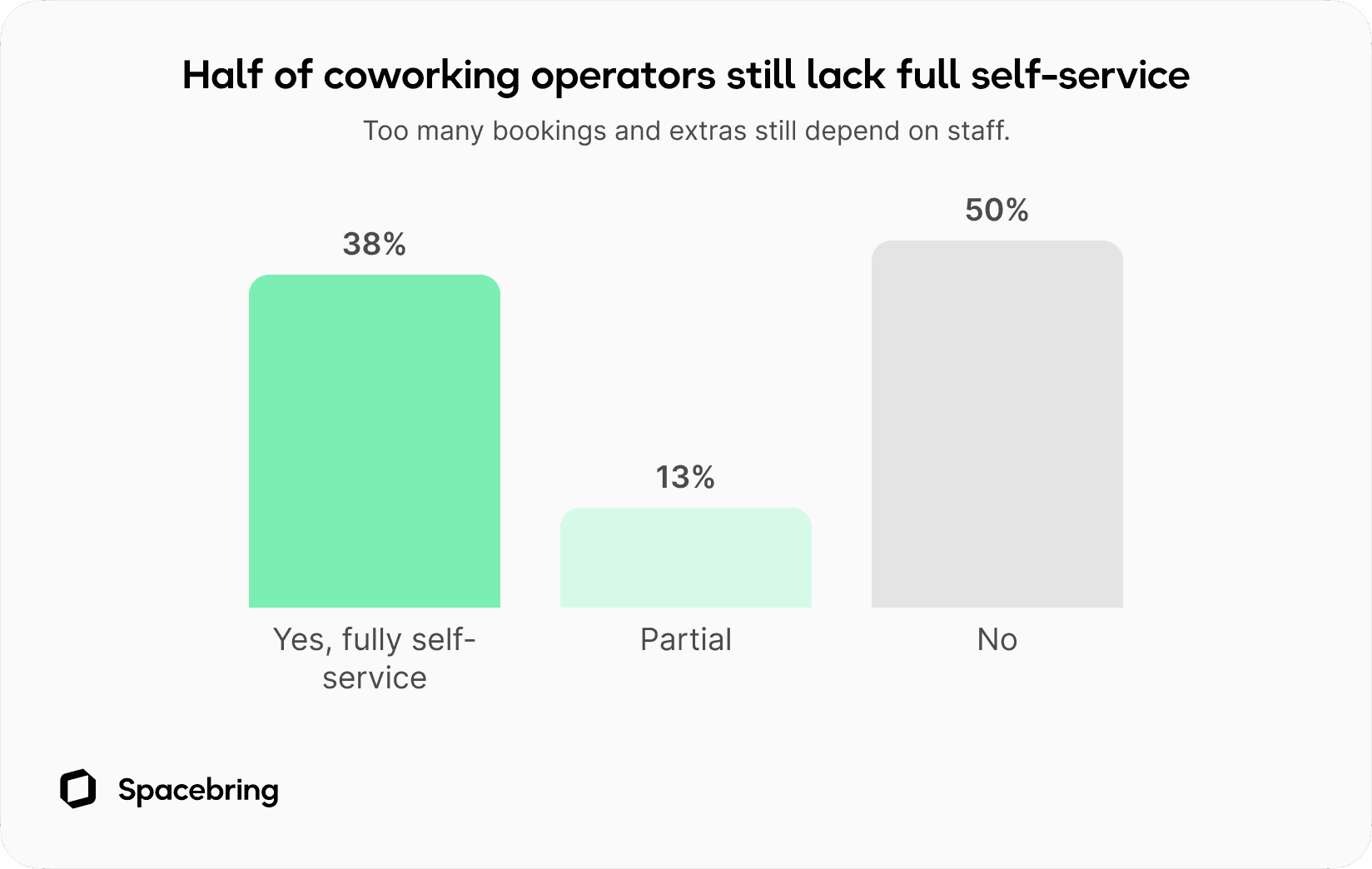

3. Self-service is still weaker than it should be

Percentages may not total 100% due to rounding.

We also asked:

Can members self-book a room, catering, and guests without admin help?

Here is what we found:

- 38% said yes, fully self-service

- 13% said partly

- 50% said no

Half of respondents still rely on staff, email, or front-desk support for tasks that should usually be simple.

That matters more than it first seems. Every manual booking request creates another interruption, another follow-up, and another small piece of admin someone has to absorb.

What this finding means

If member actions still depend on staff, growth creates more operational load.

That is the opposite of what good systems are supposed to do.

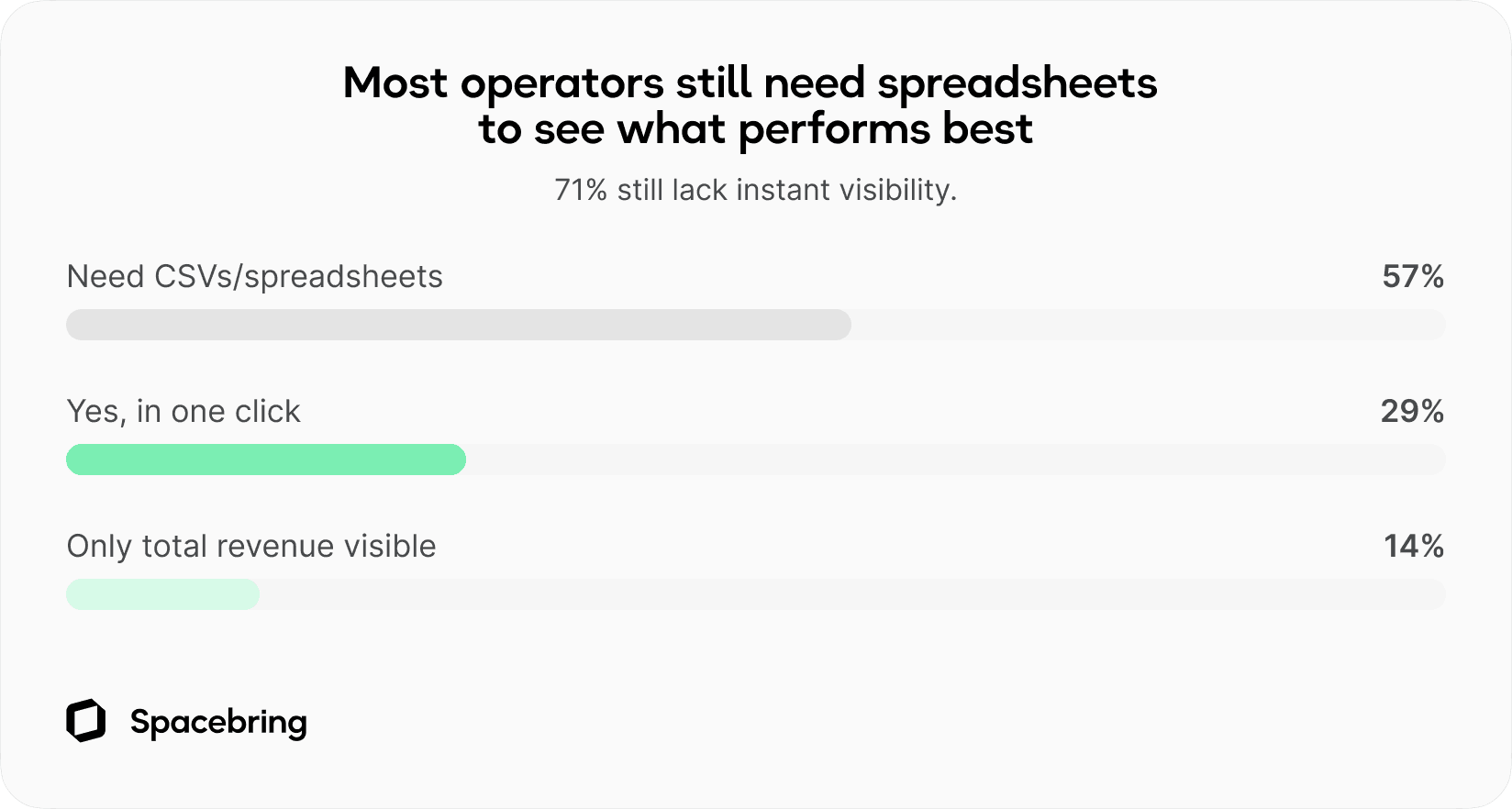

4. Reporting is still too slow for basic decisions

This may be the strongest signal in the whole dataset.

We asked:

Can you see your most profitable room or resource in one click?

The answers:

- 29% said yes

- 57% said no, they export CSVs and use spreadsheets

- 14% said no, they only see total revenue

So 71% do not have instant visibility into resource-level performance.

This matters because coworking and flex space operators make pricing and planning decisions all the time.

- Which room performs best?

- Which resource is underused?

- Which add-on drives revenue?

- Where should prices change?

- What deserves promotion?

If those answers still require exports and spreadsheet cleanup, decisions get slower.

What this finding means

You cannot improve what you cannot see quickly.

Right now, too many operators still have to work too hard just to answer basic performance questions.

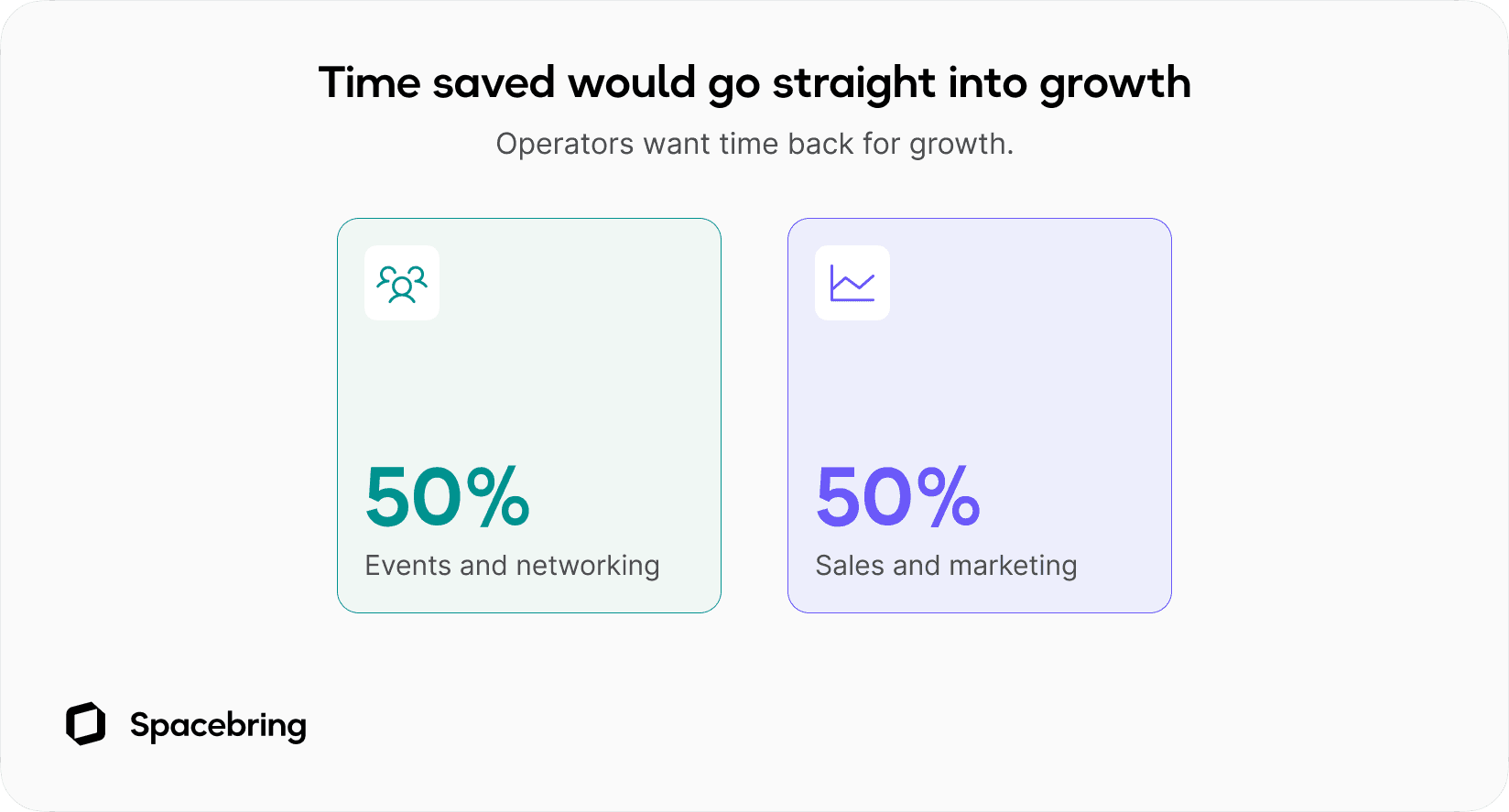

5. The time saved would go straight into growth

Finally, we asked:

If you saved 10 hours a week with tech, what would your team do instead?

The answers were telling:

This is one of the most useful findings in the whole piece.

Operators are not asking for efficiency because they want nicer workflows on paper. They want time back for the work that fills spaces, builds community, and grows revenue.

What this research says about coworking space software

This is not just a story about operations. It is also a useful lens for evaluating coworking management software.

The biggest gaps in this research are not vague complaints about “tech.” They are specific failures to fully remove manual work in four areas:

- billing

- self-service

- reporting

- cross-system workflows

That is what makes this useful beyond the survey itself. It helps explain why coworking and flex space operators can still feel friction even when they already have software in place.

A strong coworking space platform should not just look good in a feature list. It should reduce app switching, reduce billing cleanup, reduce admin-assisted bookings, and reduce the need for spreadsheet reporting.

For operators comparing tools, the better question is not “which platform has more features?”

It is:

Which platform removes the most routine work from the team?

In practice, that usually comes down to four things:

- fewer systems to manage

- less billing cleanup

- stronger self-service

- faster answers from reporting

Discover how hundreds of spaces worldwide unlock success and grow better with Spacebring

What coworking and flex space operators should do next

The lesson here is not “buy more software.”

It is to audit where time is still leaking out of the business.

A practical place to start:

- List the workflows where staff still step in manually.

- Identify the booking flows that still depend on admin help.

- Map how many tools are involved in one typical member journey.

- Check how long it takes to answer a simple profitability question.

- Measure improvement in time saved, fewer interruptions, and better confidence in the system.

The biggest opportunity may not be adding something new.

It may be simplifying what is already there.

FAQ: direct answers for coworking space owners

Why do coworking operators still use multiple apps?

Usually because one platform does not fully cover billing, bookings, reporting, communication, and access control well enough on its own. The problem is not the number of tools by itself. The problem is when staff have to manually bridge the gaps between them.

What is operational friction in coworking?

Operational friction is the extra admin created when software and processes do not fully remove manual work. In coworking, that often means invoice fixes, admin-assisted bookings, spreadsheet reporting, and switching between multiple systems to complete one task.

What should coworking operators look for in software?

Based on this research, the most useful test is whether the software reduces routine work in the real world. The strongest signs are fewer manual billing fixes, stronger self-service, less app switching, and faster reporting.

Why does reporting speed matter so much in coworking?

Because operators make constant decisions about pricing, rooms, resources, promotions, and occupancy. If those answers live in CSV exports and spreadsheet cleanup, decisions are slower and opportunities are easier to miss.

What would operators do with more time?

In this research, they said they would put it into sales and marketing or events and networking. In other words, the time saved would go straight into growth.

Methodology

This research combines:

- a focused survey of UK coworking and flex space operators

- broader insights shaped by around 200 operator conversations

- discussions at FlexSA and London Coworking Assembly events

- in-person visits and direct conversations inside coworking spaces

- additional market context from the Instant Group’s UK flex market overview

Data and insights provided by The Instant Group are compiled from their proprietary flexible industry database, providing a comprehensive, aggregated market view of flex market demand.

The percentages in the charts reflect responses to specific survey questions. The broader conclusions were also informed by recurring patterns that came up repeatedly across operator conversations and visits.

Source notes

- Survey source: Spacebring operator survey

- Market size reference: CoworkingCafe Q1 2026 UK & Ireland report

- Additional pricing and demand benchmarks: the Instant Group market overview

- The Instant Group interpretation quote: supplied by the Instant Group for this report

Credits and thank you

This piece would not exist without the coworking and flex space operators who shared their time, honesty, and practical experience.

Thank you to everyone who filled in the survey, spoke with us at events, shared their perspective directly, or welcomed us into their spaces.

Special thanks to the Instant Group for providing additional UK flex space market data and commentary used in this research.

Participant credits

- Roland Stanley, Dragon Coworking

- Nick Keynes, Tileyard London

- Jane Erasmus, UBCUK

- Simon Cracknell, Parallel Business

- Heather Taffinder, Workspace Hub

- Oliver Corrigan, Work Well Offices

- Jenny Hardaker, WCR Space

- Daryl Willcox, Jetspace

Some contributors preferred not to be named publicly. We are equally grateful for their input.

Final thought

Coworking and flex space operators do not need more complexity.

They need systems that quietly remove routine work, make reporting easier to trust, and free the team up for the parts of the job that actually move the business forward.